Ultimate YNAB Review and How To Start: Best Budgeting App 2019

This is the most comprehensive review of You Need A Budget (YNAB) you’ll find on the web.

In this guide, you’ll learn everything you need to know about YNAB, whether or not it’s right for you, how to set it up, and common pitfalls people face when starting YNAB.

If you’ve ever been:

Frustrated by trying to make a budget work

Ticked off at software that won’t do what you need

Discouraged because managing your money just isn’t working

You need to try YNAB.

Before I Start the Review

I want you to know that I don’t make a single dime from this article. YNAB doesn’t pay me anything review their product or recommend it. I’ve been a happy customer for almost a year now and really believe in the product.

In order to try and keep this review as unbiased as possible, I’ve included a review of all the major negative aspects of using YNAB. I cover both the pros and cons and make it very clear that YNAB isn’t for everyone.

I’ve included the facts about specific features and my own opinions about why you should or shouldn’t use YNAB.

This review guide is extremely long. This is not just a product review. I include a guide for getting started, pitfalls people face with the software, the YNAB philosophy, and a specific checklist for why you shouldn’t use YNAB.

YNAB Review

Cons – The Stuff YNAB Isn’t Great At

I want you to understand that YNAB isn’t perfect and definitely has some major drawbacks. Although I’m a huge fan of the software, it has flaws that you should know about. I always like to start with the downsides because it’s the most honest way to write a solid review.

Con #1 – Lack of Reporting

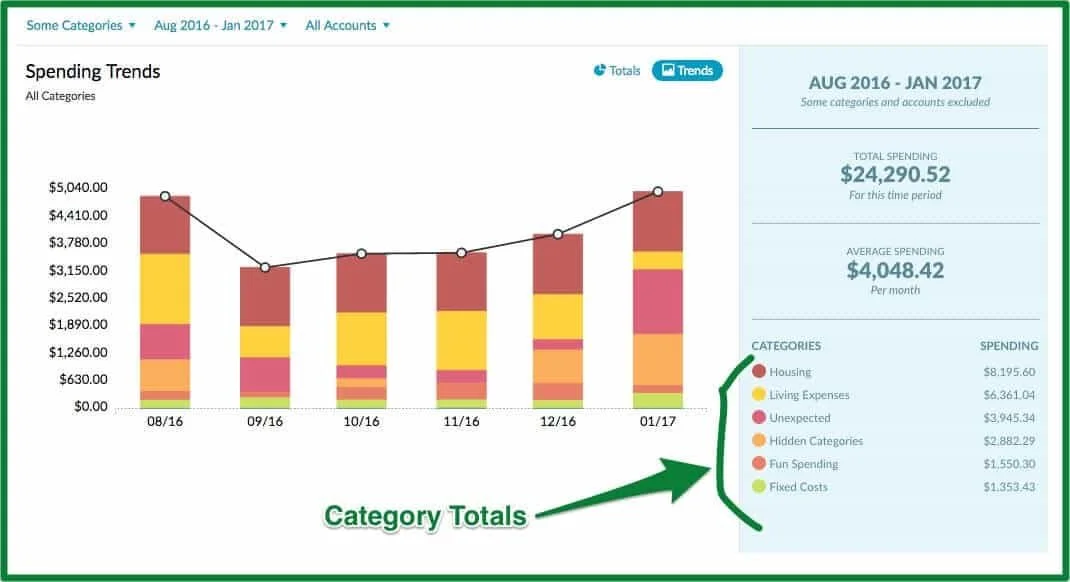

This is probably the thing I’m personally most frustrated with. YNAB has extremely limited reporting features. There are currently three major reports: Spending, Net Worth, and Income vs. Expense.

The spending report is actually pretty helpful. It’s a pie chart that shows spending by category and sub-category. You can click each category to drill down further and eventually see the individual transactions. You can also change the dates, accounts, and include/exclude specific categories. This feature is helpful to see where your money is going from month to month.

You can also look at spending over time by switching the view to a bar graph. This lets you easily see how your spending has changed from one month to the next.

Although the spending report is helpful, it’s the only one that is. The other two reports are extremely lacking.

The net worth report is just a simple bar chart that shows assets and liabilities for each month. It doesn’t show you categories of assets or liabilities and you can’t drill down into the information. If you’re interested in tracking your net worth, I would recommend Personal Capital.

The third report shows your Income vs. Expense. This is the closest YNAB gets to organizing different income sources. Since YNAB is philosophically focused on planning your expenses, it intentionally avoids income reporting. There’s not much to this report. I’ve found the most helpful column is the “average” for each category. After using the software for 6 months or more, the average is helpful for understanding your normal spending habits.

YNAB doesn’t let you create your own custom reports, have any tax-related reporting, or income reports. If you’re nerdy and want to drill down deep and analyze the crap out of your finances, the lack of reporting is going to frustrate you to no end.*

*It should be noted that YNAB is constantly updating their features and work hard to improve the software. They may introduce more reports in the future, but currently, this is all they have.

Con #2 – Terrible for Holistic Financial Overview

Due to Con #1, YNAB doesn’t do a good job of showing your overall financial health. It’s a budgeting app and is hyper-focused on that. It doesn’t care much about various sources of income or tracking other assets like your house, car, business, and investments. In fact, it’s terrible for tracking investment accounts and performance.

If you’re looking for investment tracking, net worth tracking, or a holistic financial package, I would go elsewhere. What you want is something like Personal Capital.

YNAB simply isn’t trying to be that. If that’s what you want, look elsewhere.

*However, I would like to point out that YNAB can be “hacked” to show you income and separate it out. Kathryn over at Making Your Money Matter has a great article on how she does this.

Con #3 – Phone App Isn’t Powerful (as much as I would like)

As I discuss below, the phone app is actually one of the main reasons I chose YNAB over a few other budgeting systems. It’s pretty good.

But it isn’t nearly as powerful as the desktop (online) version. You can’t access any of the reporting features from the phone app. Which means you can’t check on things like spending averages, monthly trends, or income vs. expenses from your phone.

You also can’t set your initial account up from the app version. When you get started, you have to use the online app.

The phone app is focused on letting you see your budget and enter new transactions… And that’s about it.

Con #4 – Automatic Account Import Is Clunky

YNAB was originally intended for you to enter transactions manually. This is totally different from Mint’s philosophy which is to automate as much as possible.

However, in the newest version of YNAB they’ve introduced automatic account importing. This means YNAB will pull in transactions from your bank and credit cards (if you want them to) and update your budget automatically.

While great in theory, this feature still has some bugs. It doesn’t ever update my investment accounts. I have to manually check what my investment account balances are and then tell YNAB to update my balance. This kind of ruins the entire point of having automatic import.

YNAB is a little better at importing transactions from your banks and credit cards. But you still must update your budget manually and verify everything was categorized correctly. Renee over at Tune My Heart explains this process as semi-automatic.

If you want software that automatically pulls in everything for you, and requires no work on your part, YNAB won’t make you a happy camper.

Con #5 – Dealing with Reimbursements can be Annoying

I should tell you that YNAB actually handles reimburse-able expenses and reimbursements better than most other apps. I used to use Quicken for Mac, and it was TERRIBLE about handling reimbursements.

But still, YNAB could be better.

I travel for work often and put all of those expenses on my own credit card. Then my employer reimburses those expenses within a week or two. I also periodically buy things for friends or family and then they pay me back.

YNAB handles this okay unless you get reimbursed in a different month than the expense occurred. Due to YNAB’s philosophy of budgeting every dollar before you spend it, this causes an issue.

Since I normally don’t know what my travel expenses will be until after I spend them YNAB constantly thinks I’m overspending.

If I get reimbursed during the same month, this is fine. I just tell YNAB that new income will cover my “over” spending. But if I travel during the last week of the month and don’t get reimbursed until next month, YNAB can’t handle this. Since it wants me to budget for expenses on a monthly basis, it won’t let me carry expenses forward.

This means I have to change the date of the reimbursement to the last day of the month.

EXAMPLE:

I spend $200 on January 27th for a hotel in CA. My employer deposits $200 into my checking account on February 7th. Although this is how it happened in real life, I will tell YNAB that my employer deposited the reimbursement on January 31st. This makes YNAB happy and balances my budget for January.

You can work around this problem by doing what I describe above, but it’s annoying.

Con #6 – YNAB Isn’t Free (It’s a subscription… like Netflix)

I discuss this in more detail below but unlike other budgeting apps, YNAB isn’t free. And unlike other budgeting programs, YNAB isn’t a one-time cost.

It’s currently priced at $5/month or $50/year if you pay for the year in full. While this isn’t a major expense, it does feel funny to pay for software that’s supposed to help you save money… right?

However, YNAB does have a good reason for building their business on this model. But the fact is, it isn’t free, and that’s a major downside for lots of people.

Con #7 – Can’t Carry Negative Balances Forward

One of the best features about YNAB is that it lets you carry positive balances on categories forward to the next month.

For example, let’s say I have a category for eating out of $100/month. And in January I only spend $75. That means in February, I can spend $125 on eating out! It lets me keep the money I didn’t spend from January.

A lot of budgeting apps don’t let you do that, and it’s a major pro for YNAB.

However, they DON’T let you do the opposite. If you spend $125 in January, it won’t make you spend only $75 in February. If you go over budget in a single category, YNAB makes you fess up and cover that overspending with money from another category before moving to the next month.

I understand this is simply based on the beliefs behind YNABs core budgeting philosophy. But personally, I would like to be able to carry negative balances forward… As you might guess, this would fix the problem of reimbursements I pointed out in Con #6 above :).

Con #8 – Getting YNAB set-up can be confusing

I discuss this in greater detail below. But you should know that when you use YNAB for the first time, you will likely have a lot of questions. Luckily, they do have great customer support and good educational tools that will help you. I certainly emailed their support A BUNCH when starting out.

Once you get the hang of its quirks, it’s not too bad. But it’s definitely a downside when you’re getting started.

Pros – Stuff That Makes YNAB Standout

Now that we’ve covered the biggest flaws, let’s talk about what makes YNAB my favorite budgeting software.

Pro #1 – The Company Mission

One of the things that make YNAB standout is their hyper focus on you and me, the user. Their mission is to “help you stop living paycheck to paycheck, get out of debt, and save more money faster.” The entire system is built on zero-based budgeting. That just means YNAB wants you to think about every expense from the ground up. That’s very different than most budgeting apps that just based your budget on what you did last month.

Which brings me to the next point.

Pro #2 – YNAB Focuses On Moving Forward – Not Looking Backwards

YNAB is built on the idea that every dollar needs a specific job. The software doesn’t track your different sources of income, and instead puts it all into one pile: “To Be Budgeted”

Every time you get paid that money goes into your “To Be Budgeted” pile and you then tell it where to go. In this case, you might send $300 to groceries, $50 to pet expenses, and $50 for spending money.

A lot of budgeting apps let you set up a monthly budget and then they try to make you hit that every single month. Or they just track your expenses and let you look at reports after your spending has already happened. YNAB proactively helps you decide where to spend your money before you spend it, every single time you get paid.

Pro #3 – They Know Your A Real Person, With Unexpected Life Circumstances

Before I used YNAB, I tried all kinds of different budgeting apps. But I kept getting frustrated because they wanted me to set a monthly budget and then stick to that every single month.

But that isn’t realistic!

Some months I have more birthday gifts to buy. Sometimes I want to go out to eat more. And other times I have unexpected car trouble. Budgeting months are like snowflakes, there’s no two alike.

Let me say that again.

Your Monthly Budgets are snowflakes, there are no two alike

YNAB knows this and built this human element right into the software.

Whenever you go over in a certain category, the software notifies you.

Then they ask how you want to cover that overspending. It’s super easy to transfer money from one category to another. If I go over in groceries, but I’m under in unexpected, I can use the unexpected money to cover my grocery bill.

Using excel, or changing the monthly budget entirely is a major pain when transferring money from category to category.

Honestly, this feature alone makes YNAB worth it.

Pro #4 – Completely Customizable Categories

A lot of the budgeting apps out there have pre-defined categories that you must work within. But again, you’re a human. You’re unique and have unique needs. You probably don’t fit neatly into these pre-defined categories.

I sure don’t.

YNAB lets you have full control on how many categories and sub-categories you have, the names of those categories, and how they should be organized. This is especially helpful when you’re budgeting for something specific like a vacation or have reimbursable expenses through your employer.

For example, some of our more unique categories include “winter western vacation,” “Nick’s work reimburse-ables,” and “puppy savings.”

Pro #5 – Handles Irregular Income with Ease

Since the software has you budget money as it enters, irregular income isn’t a problem. With normal budgeting software, you’re supposed to budget your expenses for the entire month before you get paid.

But this is a problem if your income isn’t always exactly the same. And for many people, it isn’t. In 2016, 34% of the U.S. workforce were freelancers. And that number is on the rise. But even if you aren’t freelancing, you might get paid overtime, or work multiple jobs. Mine and Hanna’s income can vary widely from month to month, so having a system that handles this easily is a must.

Pro #6 – Customer Support Is Top Notch

I’ve written into customer support quite a few times over the last 8 months and had a great experience each time. This is something the YNAB team prides themselves on and they take it very seriously. I’ve emailed them with a variety of issues ranging from complex to just saying hey.

Here’s the breakdown of my customer support interactions:

July 21st, 2016

I wrote in because I was having trouble understanding the way credit cards were entered when you first set the software up. My question was horrible. I didn’t even know how to ask it correctly because I was so confused.

We sent back and forth emails for 5 days and they helped me work through all of my issues. Which was mostly just me misunderstanding. They also pointed me to some really good resources on understanding this. I share this below in the section on setting up credit cards.

Complexity of my issue: 10/10

Avg. Response time between emails ~20hrs

Ability to solve my problem ~ 100%

Tone and Niceness ~ Grade A

October 24th, 2016

They had just released their reporting function. Before this, there were not reports at all. Here’s the email I sent.

I was just really happy.

They emailed me back in 4 minutes.

Complexity of my issue: 1/10

Avg. Response time between emails ~ 4 min

Ability to solve my problem ~ 100%

Tone and Niceness ~ Grade A

January 23rd, 2017

I wrote in to tell them that I really liked the spending reports but would love it if they added some income reports (see my con #1 above). Brittany sent me back a really nice email explaining the reasoning YNAB doesn’t have these reports.

Although I personally would like to have income reports, I understand their reasoning. And I think it’s great that they take the time to explain this to anyone who writes them… Even though it’s all over their website. Brittany didn’t slam that up in my face, she just explained in a really nice tone without calling me lazy for not reading the dang website.

Complexity of my issue: 2/10

Avg. Response time between emails ~ 1 hr

Ability to solve my problem ~ 100%

Tone and Niceness ~ Grade A

The bottom line is that their customer support is very responsive, good at answering your questions, and treats you like a real person.

Pro #7 – FREE First Year for Students

Although YNAB is $50/yr for normal members if you’re currently a college student (or high school) you can get your first year of YNAB for free!

All you need to do is send them an email proving that you’re a student.

Pro #8 – Ridiculous Amount of FREE Education

One of the things that YNAB does extremely well is their solid education around personal finance. A lot of the budgeting tools have blogs and free resources, but none of them hold a candle to YNAB.

They have a podcast, a super helpful weekly video show, free weekly live classes with Q/A, in-depth guides on specific finance topics, and extensive documentation on setting up YNAB.

Of course, you could use all of these resources for free without being a customer.

And that would be fine.

But I point this out because all of this content goes to further support YNAB’s core mission of actually trying to help people get better with money. Sure, they’re a business and have to make a buck or two. But they put their money where their mouth is when it comes to serving you and me.

Pro #9 – Supports and Encourages Manual Entry

This pro is definitely my opinion. Some people won’t care about this feature at all.

YNAB was built on the idea that you should enter your transactions by hand instead of automatically importing transactions. Manually inputting your transactions forces you to be more aware of your money as you spend it. When you automatically import, you may not look at your budget until halfway through the month.

By that time, you’ve probably already blown more than you should have.

While YNAB does allow you to automatically import transactions, it also has a super clean setup for those who want to do it manually. Like me.

Both Mint and Personal Capital want you to use their importing functions and any manual entry is really difficult to work around.

You might be asking “If I’m going to enter everything manually, why the crap wouldn’t I just use a spreadsheet.”

The answer is because YNAB still makes things 1,000% easier than a spreadsheet. Because of the mobile app, whenever I buy something I literally enter the transaction as I’m walking out the door of the store/restaurant on my phone. It takes very little time and it pushes the update to my wife’s phone as well so that we both are always aware of the budget. Unlike when we used to use Quicken or Excel and it was only on my laptop.

Top YNAB Features – The Facts

So we’ve covered the pros and cons of using YNAB. But there are still some features I didn’t include above. If you’re familiar with budgeting and software options available, this section is for you. Below I point out some of the top features and functions that YNAB supports. If you’re looking for software that does something very specific, read this section.

Top Feature #1 – Security is Standard For Financial Software Products

They keep all of your information encrypted and fully secure, according to their security policy you can check out here. PC Mag has a great article explaining in a little more detail YNAB’s security. Essentially, they follow the major industry protocol for encrypting and securing consumer financial information.

YNAB doesn’t offer a multi-factor identification method (like getting emailed a specific access code every time you log in). I’m sure part of their reasoning is providing convenience for the end-user. I certainly would be ticked off if every time I wanted to check my budget I had to enter an extra access code they just emailed to me.

But, if extra super crazy tight security is important to you, then maybe budgeting through an app isn’t what you want.

Top Feature #2 – Syncing Between Phones and Desktop

YNAB allows you to enter transactions through the phone app whether or not you have an internet connection. Which is HUGE. I don’t stay connected to data all the time, so when I’m not on Wifi, some budgeting apps are a problem.

Whenever you connect to the internet and open YNAB, it will push any transactions you entered on your phone to the online app (read: cloud). It will also download any transactions and update your phone app with new information.

So if Hanna goes and buys groceries at Walmart, while I’m at Costco, she can push her transaction to the cloud and I can see what’s left in the grocery budget as well. This feature alone is one of the major reasons I love YNAB. Hanna and find this SUPER helpful.

Top Feature #3 – Allows You to Set Specific Goals

Not only does YNAB help you stay on budget and within your categories, they also help you set and achieve specific goals.

You can easily set a new goal to pay down debt, spend a certain amount, or save a to a specific number and YNAB will remind you of your goal every single month. If you’re trying to get out of debt or save for something big, this feature is great for setting up your own personal accountability partner.

Top Feature #4 – Search Bar

This feature is actually pretty new. But you can now search by category, account, payee, or even specific words you typed in the memo line. I use this all the time when I’m checking on how much money I really spent buying unnecessary crap on Amazon 🙂

If a budgeting app doesn’t have a search function, honestly, it’s usefulness drops so much I almost wouldn’t even want to use it. This feature is a must have.

Top Feature #5 – Easily Splits Transactions

You know how last time you went to Costco to get eggs and milk, and then somehow came out with $200 worth of who-knows-what?

Well, YNAB lets you deal with that.

Whenever you spend from multiple categories on one transaction, you can easily split that transaction and tell YNAB to take money from different categories to cover the spending.

So milk and eggs goes under groceries, and those clothes, oversized box of popcorn, and all the seasons of Gilmore Girls goes somewhere else 🙂

Top Feature #6 – Allows For Quick Reconciliation

If you’re not familiar, reconciliation is a process that helps you make sure that what your bank account shows is actually what happened. Your grandparents called this “balancing the checkbook.”

When keeping track of your budget you need to make sure that your actual accounts and tracking accounts agree. A lot of software (ahem, Quicken) have a complicated reconciliation process where you look at statement balances and enter multiple numbers. It’s a pain.

YNAB makes it simple by letting you checkmark each transaction when it hit your account and then click the reconcile button if the account balances match. YNAB always shows you the cleared balance (what you’ve accounted for in the real account) and the working balance (what YNAB shows is the balance). When all of the transactions are accounted for, these two numbers will match.

When you checkmark a transaction it adds it to the “cleared” which means the transaction has posted to your account. Then when the “cleared” balance matches the actual account balance (check this on the specific website of your bank/credit card etc…) you can hit the “reconcile button.”

Top Feature #7 – Sync Bank Accounts and Credit Cards

Although YNAB does have some issues syncing investment accounts and updating your information based on daily stock fluctuations, it syncs well with banks and credit cards.

Personally, I don’t do this. I think there’s a big benefit by manually entering all of your transactions. But I recognize that a lot of people want to sync automatically. It’s a hassle to enter everything manually. If that’s you, have no fear, YNAB does let you sync.

Top YNAB Features – My Personal Favorites

I covered some of the most popular features above. But I wanted to create a second list and share why I specifically chose YNAB. I’m extremely picky when it comes to my financial software and there were a handful of things that really stood out to me and made YNAB the winner.

My Favorite Feature #1 – Separation of Budget and Non-Budget Accounts

This.

This. Freaking. Feature.

Incredible.

Seriously, this feature alone probably could have sold me on YNAB. It’s a nuanced thing, and so you may not understand the significance of it at first. Let me explain.

Most financial budgeting/tracking software (think Mint and Quicken) look at all of your financial accounts together. Your checking, credit cards, savings, investments, and retirement accounts are all in one house. The problem with this approach is that when you transfer money between accounts, the software shows that you haven’t spent the money.

And technically you haven’t.

But that’s a problem if you want savings to be part of your budget. For instance, let’s say that you want to save $100 per month for your vacation next year.

You get paid on Friday and the money goes to your checking account. On Monday you transfer $100 from checking to vacation savings. But because you never spent the money, your budget shows that you never “saved” that money. Since you just transferred it from one account to another it hasn’t been spent.

Here’s a diagram to help you see what I mean.

This is how a lot of budgeting software handle transfers. Which is a major pain if you want to actually track how much $$ you’re saving.

YNAB doesn’t do it this way.

Instead of looking at all of your accounts as one, YNAB lets you separate budgeting accounts from non-budgeting accounts. They call these non-budgeting accounts “tracking” accounts. Their things you still want to keep track of, you just don’t want them inside the budget.

Here’s how my accounts are currently set up:

By doing this your budget ONLY counts what happens inside the budgeting accounts. So if I had a savings account that was also a “budgeting” account, then YNAB would do what the other programs do.

But since my savings accounts are “outside” my budget, when I save the money, YNAB sees it as gone from the budget.

This is huge. Honestly, I don’t know why all budgeting apps aren’t doing this. This is an easy problem to fix, but again, YNAB pulls through as one of the only apps who understands what happens in real life.

My Favorite Feature #2 – Carry Over Excess Money From Month to Month

If the inside/outside budgeting accounts feature wasn’t enough to make me use YNAB, this feature pushed me over the edge.

Again, YNAB understands that every month is different. You may not spend as much money eating out this month as you want to next month. So the software lets you use any excess budgeting money in the next month.

This is especially helpful for “spending” money.

Hanna and I currently give ourselves both $45/month for guilt-free-buy-whatever-you-want spending money. But sometimes I want something that costs more than $45. In order to get it, I will spend less money for a month or two and save my spending money over time. Then when I have enough to buy what I want, the spending money is there for me to get it.

We used Quicken for the first couple years of our marriage and it wouldn’t let us build up a category over time like that. Which sucked.

I ending up having to generate special reports and do weird workarounds to keep track of how much spending money with both had. YNAB solves this problem by just rolling any leftover money in a category over to the next month.

Huge.

My Favorite Feature #3 – Handles Reimbursements Fairly Easily

You’ll notice above that handling reimbursements is also in my cons section of this review. To be honest, my relationship with the way YNAB handles reimbursements is bitter-sweet.

It does a WAY better job of handling reimbursements than other platforms because YNAB lets you budget different amounts every single month. Lots of programs want you to set a monthly budget and then use that same budget every single month.

That’s a problem for anyone who travels for work. As you know if you travel a lot, your spending is all over the place. Some months I may have $500 worth of reimbursements from my company. Other months I’ve had as much as $4,500 in a single month.

I just keep track of my spending when I travel for work and then submit an expense report when I get back in town. I make sure and enter the transactions in YNAB under my “work reimbursements” category. Then once my company pays me back, it’s easy to send that money to cover the spending.

If you travel a lot for work, this feature is a must have.

But again, my only pet peeve is not being able to carry spending from month to month. See Con #5 above for more details.

My Favorite Feature #4 – Phone App Lets Me Always Know What The Budget Is

I know I said this already. But this feature really is huge. YNAB shows you the budget even if you don’t have internet access. Then when you sync back up to the internet, it will refresh and give you the latest information.

This is a huge improvement over using spreadsheets and other desktop applications. With the phone app, Hanna and I are always on the same page. I included it here because it was one of the major factors in our decision to use YNAB.

How YNAB Actually Works

Remember, YNAB is built on zero-based budgeting. If you’ve ever heard of Dave Ramsey and his envelope system, you’re already somewhat familiar. If not, let me explain.

I mentioned this as Pro #4 above, but YNAB lets you customize your budgeting categories into two levels.

Category Group

Category

With category group, you can put all of the similar categories into one area. The main purpose of grouping them together is to make reporting easier.

“Ok, ok, ok, that’s categories. But how do you actually USE it?”

Glad you asked.

Process Flow For Using YNAB

Using YNAB is extremely easy. After you set up your categories, moving forward is a simple four step process.

Step 1: Enter income transactions as “to be budgeted.”

This money will now be available in a big green box on your budget page. The box lets you know that you need to tell this money where to go.

Step 2: Tell all of your to be budgeted money where to go (green means you have money left to spend).

Once you assign money to specific categories, that category balance will turn green. If the category is green, it means you have that much money left for the rest of the month. If you go over, you’ll need to send more money to that category.

Step 3: Spend your money and enter transactions as you go.

Step 4: Redistribute money from one category to another as the month progresses and your budget changes.

That’s it.

YNAB Wants You To Stop Living Paycheck to Paycheck

The last thing you need to understand about YNAB is a concept called “aging” your money.

I know, weird.

In the top right-hand corner of your budget screen is a number of days and a title called “Age of Money.” This is the number of average days between money coming in and money going out.

Think of it as the number of days between when you get paid, and when you need to get paid again.

If this number is zero, that means you’re literally spending your entire paycheck on the day you earned it.

Ideally, YNAB wants you to get to 30 days. When you reach 30 days it means that an entire month is going by before your spending that money.

“how the crap can I go a whole month without spending.”

Great question!

YNAB lets you budget ahead of time.

Let’s say you get paid on January 1st and again on January 15th. You send all of that money to your specific categories but then notice you’ve budgeted everything you planned for and still have $200 left over.

Instead of just spending that $200, you can actually go forward to February and budget that $200 for next month.

By doing this over and over again, you will eventually be able to budget the entire month of February with January money.

This lets you stop spending money on a credit card knowing that you’re going to get paid next week.

Before using YNAB I still always paid my credit card in full, but I budgeted based on what my salary was. I would plan the month out before I received any money and start spending. Then once I got paid, I could pay off the credit card.

While that works in theory, YNAB forces you to try and get a month ahead. Which is HUGE and a much better habit to get into.

Not to mention, if I ever got fired while doing my old system, I would’ve had a month of expenses on a credit card that I couldn’t cover.

If You Want More Info On The YNAB Process

Keep reading.

I go over the strategy and philosophy of YNAB below.

But if you’re serious about using this software, I highly encourage you to check out YNAB’s Youtube page and specifically, their getting started video which I’ve linked up here.

YNAB Costs

Unlike some of the other popular budgeting apps (mint), YNAB isn’t free to use. They have a 34-day free trial which lets you get through an entire month of budgeting. After that, it’s $50/yr.

You might think it’s ridiculous to pay for a service that’s supposed to be helping you save money… After all, couldn’t you just save money by not paying?

Maybe.

But you should know that on average new YNAB users are saving $200 in their first month and several thousand throughout the year. So a measly $4.17 a month certainly seems worth it.

The other reason I’m personally willing and happy to pay is because it’s a better pricing model than alternatives. This subscription model has 2 major advantages:

Number 1: YNAB doesn’t need to make money in other ways like advertising and pushing products.

Mint and other free apps still have to make money. Normally, the way they do this is by placing ads for credit cards, loans, and bank accounts that you don’t need. And even worse, a lot of these products are actually bad for your financial health. Yet these apps that are supposedly trying to help you, push these products because they need the money.

Number 2: YNAB has a constant and steady stream of income that allows them to build new features quicker.

Since switching to a subscription model YNAB has been able to iterate and improve much faster than they used to. Like Netflix, with a steady stream of income, the YNAB team has been able to hire more developers and implement better features that actually help the end user.

The CEO at YNAB wrote this article explaining how they can roll out new features (like better reporting, mobile update, etc…) faster since switching.

So yes, the software isn’t free. But it’s a lot of bang for your buck.

Bottom Line Benefits for Every-Day People

At this point, you can probably tell that I’m a huge fan of YNAB and I make no bones about it. I think it’s currently the best budgeting software on the market and you’re crazy not to at least try it.

If I had to boil the major benefits down into just a couple of bullet points, I would say it like this.

YNAB is a killer budgeting app because:

Simplicity – YNAB is easy and intuitive to use

Saves You Money – The YNAB system has consistently proven to save people money

Saves You Time – YNAB saves time by using a mixture of automation and manual work

Phone App – The app keeps you informed on where your money is and how much is left

Education – The customer support and education in the community is unparalleled

Realness – YNAB knows you’re a real human with unexpected changes, and it compensates for that

If you’ve made it to this point in the article, you should probably go ahead and sign up for the free trial.

YNAB Philosophy

At this point, I’m done writing the YNAB review. If you have more questions, please leave a comment below.

Next, I want to focus on the philosophy behind YNAB. If you want to use YNAB you have to understand the beliefs that it is built upon. Because if you don’t buy into these core beliefs, YNAB isn’t going to work for you. In order to get the maximum value out of YNAB, you can’t do it halfway.

You’re either in or you’re out.

That being said, YNAB has four rules for budgeting. Here they are:

Rule #1: Give Every Dollar a Job

The first rule is fairly straightforward. As money comes in you must assign it to a category of spending/saving.

Instead of leaving that $500 paycheck in your checking and assuming you have lots of money, you must tell every single dollar what category it should be used for.

$50 for clothes, $200 for groceries, $45 for spending etc…

You can’t let your money sit, even if you leave it in your checking account, you must give it a job.

Rule #2: Embrace Your True Expenses

Rule number two is all about recognizing that you’re a human, not a freaking robot.

You have unexpected and irregular expenses. This includes things like car maintenance, insurance premiums, and Christmas shopping. YNAB helps you embrace those costs for the year by helping you set aside a certain amount every single month.

I cover this concept in more detail in this article.

For example, Hanna and I do this with Christmas. We currently set aside $100 every single month for Christmas shopping. That takes care of presents, decorations and extra food for hosting people. So when December rolls around we have plenty of money instead of needing to use a credit card or dip into the emergency fund.

Rule #3: Roll With The Punches

The third rule is by far my favorite and one of the biggest reasons I use YNAB.

Like I’ve said before, a lot of budgeting apps set a strict budget every single month and don’t allow you to easily change it.

YNAB is different.

They understand that your month to month expenses will always be different. So the software lets you easily take money from one category to cover overspending in another.

Instead of beating yourself up every time you overspend on groceries, just recognize that it’s life and use money from another category to cover it.

No big deal.

As Four Year Strong would say: “Roll with the punches cause you know that it’s inevitable.

Rule #4: Age Your Money

The last rule is all about using last month’s money for this month’s spending.

I covered this extensively above, so I won’t go into detail again. But YNAB encourages you to stop living paycheck to paycheck by showing how many days go by between money coming in and money going out.

This is a huge benefit when you get there. By consistently living on last month’s income, you’re able to stop living paycheck to paycheck and get a much better handle on what your money is actually doing.

As a result, stress levels go way down 🙂

YNAB Probably Isn’t For You If….

While I really like YNAB, it’s definitely not for everyone. I’ve covered a lot of these reasons in the review above, but I want to have one single place with all of the reasons you shouldn’t use YNAB.

If you fit any of these, you may want to look for a different piece of software.

You Don’t Buy The Philosophy

If you read through the four YNAB rules above and scoffed, YNAB probably isn’t for you. YNAB relies on these rules for everything they do. If you have a better system that works, then great! This just isn’t the software for you.

You Want To Track Investment Performance

YNAB is a budgeting app and doesn’t focus on investments. It does let you add investment accounts to look at, but it doesn’t show you real-time tracking, any fancy charts, or help you invest.

If you’re looking for investment tracking go elsewhere.

You Want A One Stop Shop

If you want a holistic picture of your finances where you pay close attention to net worth, investments, mortgage, car loans, and your budget, this isn’t for you.

YNAB focuses on budgeting. It knows what it’s good at and it stays in its lane.

You Want To Run A Ridiculous Amount Of Customizable Reports

You should probably just use Excel.

The reporting features on YNAB are nice and handle what the vast majority of people need. But if you’re a finance nerd, YNAB may not give you everything you want… I love YNAB, but I still use Excel to generate a couple of investment reports that I want for myself.

YNAB generates some good reports, but if you’re super hardcore, you still won’t like it.

You Want Excellent Syncing With As Little Manual Input As Possible

So… What you’re telling me is, you really aren’t wanting to budget at all are you? You just want to track.

Remember, there’s a big difference between tracking your spending and budgeting your money.

YNAB does the latter.

You Don’t Want To Pay Any Money

Like I said above, YNAB isn’t free. It does cost $50/yr.

But there’s a good reason for it.

If you still don’t feel comfortable paying and can’t stand the idea of spending money for a budgeting app, then I would go find something else.

You Want To Track Your Business Finances

If you run a small business or do freelance work, YNAB isn’t for that.

You need accounting software like Quickbooks, XERO, or Freshbooks.

I still recommend using YNAB for your personal budget. Just leave business finances to a true accounting system.

How To Get Started And Common Pitfalls

So you’ve decided you want to give YNAB a try.

Great!

Let me help you out be stepping you through a couple of things before you get going. Unfortunately, YNAB can be a bit confusing when you’re first getting everything set up. Luckily, if I can’t answer your questions here, the YNAB help docs probably can.

Here are a few things that would have helped me when I was getting started:

It Helps If You Already Know Your Baseline Spending

If this is your first time using a budgeting app or tracking your spending, it’s going to be frustrating. Give yourself a few months to understand how much you normally spend on groceries, clothes, entertainment, gas, and other household items.

If you’ve previously tracked spending or used other apps like Mint or Quicken, switching to YNAB will be a lot less painful.

But if you’ve never even tracked your spending, you should start doing that whether or not you decide to use YNAB.

Set Up Budget Accounts and Tracking Accounts Correctly

I explained the way budgeting accounts vs. non-budgeting (tracking) accounts work above. If you haven’t read that, then go back.

If you have, just make sure to double check how you set everything up.

In general, checking accounts, credit cards, debit cards, and cash should be “budgeting accounts.” These are the things you’ll use for your normal spending. Your investment accounts, retirement accounts, and savings accounts should be “tracking.” These are places that you’ll send money for savings.

YNAB will let you set up savings as a “budget” account. However, I recommend setting them up as “tracking” accounts instead. When you do this you can send money from your checking account to a savings account and your budget will show that money as being “spent.”

This is important if you’re trying to save a specific amount every month and want to make sure that you don’t spend your savings. If you’re curious about what I use for savings, check out my article on Ally bank here.

Mark All Existing Money as “Inflow To Be Budgeted”

When you first set up YNAB, you’ll likely have at least one checking account. You may have multiple and you may also have an account where you track the cash in your wallet (if you’re crazy hardcore).

Any money that you have on hand needs to be entered as “to be budgeted.” When you set up the initial account balance, YNAB will likely do this for you, but be sure to double check.

For example, if you have $500 in your checking account, you’ll enter that as the starting balance and your “to be budgeted” will increase to $500. Then you’ll need to assign that money to whatever categories you see fit.

Use Starting Balance Money to Budget for Credit Card Balances

Setting up my credit card accounts was one of the most confusing things when I first started with YNAB. Let me explain.

Let’s say you budget $400 per month for groceries.

Then you go to Whole Foods and pick up $120 worth of overpriced organic Quinoa with your Discover Card. YNAB will take $120 from your available grocery category and send it to your Discover Card payment category.

So the $120 in actual cash sitting in your checking account WAS marked for groceries, but now it’s marked for paying the credit card bill.

If you had used a debit card from your checking account to pay for the groceries, then YNAB would have just reduced the amount available in that category and your checking account balance would decrease.

But when you use a credit card, the checking account balance doesn’t decrease. The cash is still there. So in order to make sense of everything, YNAB just changes the category of that money to credit card payment.

This is a really important concept to understand and one of the foundations YNAB is built on. So spend some time here.

When you initially set up all of your accounts, you may have some outstanding balances on your credit cards. If you are planning to pay the balances in full with money in your checking account, that’s great! Just budget for that exact amount in the very first month you start using YNAB. Then after that, YNAB takes care of the credit card payment side.

But you may not be able to pay off your balances right away, and that’s okay. You’re working to dig yourself out of that nasty credit card debt.

Just send as much money as you can to the credit card payment category, and over time you’ll be able to pay down your debt.

If you’re still having trouble understanding this concept, the YNAB team has put out some really great resources you should check out here, here, and here.

Understand and Correct OverSpending

One thing that makes YNAB so unique is how easy it lets you deal with overspending.

If you overspend in a cash/debit account the available balance in that category will go from green to red.

Red is bad.

A red category means that you overspent with cash and that money is gone forever.

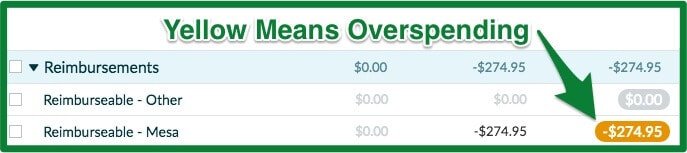

If you overspend on a credit card the available balance will go from green to yellow. Yellow is bad but not as bad as red. It means you overspent with credit and you need to cover that overspending with cash. The money hasn’t left your account yet, you just OWE that much to the credit card company.

In either case, it is an easy fix. All you need to do is click on the overspending and a pop up will ask you where you’d like to cover that spending from. If you want to use “Clothing” money to cover your extra “Grocery” spending it’s as easy as a couple of clicks.

You’re a human and you’re going to overspend. It’s okay. Just be sure to cover it with money from somewhere else.

Understand The Limitations of the Phone App

I recommend using the phone app to check your budget and enter transactions. If you’re in a pinch at a store and trying to decide whether or not you can afford those shoes, the phone app will save the day. You can pull it out and immediately know if there’s money left in the budget.

And if you purchase the shoes, the phone app will let you enter the transaction and update to the cloud!

Pretty freaking sweet.

However, when it comes to actually sending money to categories and dealing with “inflow to be budgeted,” the phone app is woefully inadequate. Plan to do most of your setup, category allocation, and budgeting from the desktop/laptop/web browser version of YNAB.

YNAB Success Stories

Now that I’ve covered an exhaustive review, some of the common pitfalls, how to get started, and whether or not YNAB is right for you, I want to end by sharing a few stories.

There are tons of success stories of people using YNAB. Heck, YNAB even has their own link to share these stories.

But I thought I would highlight a couple of stories from independent users for you to see just how powerful this software is.

Vic Says his Marriage Has Never Been Better

Vic from Dad is Cheap said that YNAB has totally changed his family’s finances. He and his wife feel more comfortable with their money and are able to talk openly and honestly now. At first, the price of YNAB was a big turnoff for Vic. But today, he says that YNAB has paid for itself many times over and that his “marriage has never been better.”

Check out Vic’s story and review of YNAB here.

Reddit User Success Stories

There is an entire subreddit full of YNAB users who help each other answer questions about YNAB. While there’s tons of useful information and folks helping each other out, there’s also lots of people posting about their own success with YNAB.

Reddit user handlebar_moustache was able to pay down his last credit card and get totally debt free in only one year using YNAB. Check out his story here.

Jamie from Two Cents Together

Jamie has one of the most inspiring stories by a long shot. While most YNAB users save $200 during their first month, Jaime actually saved $2,000!!

She says “We won’t get into the nitty gritty of the amount of money I was spending on eating out, going for drinks with friends and shopping in my first month with YNAB, but I was shocked (and a little ashamed).”

To hear more of Jaime’s story and how YNAB changed her financial life, check her out here.

Just For Fun – The YNAB Mixtape

So you’ve come to the end, and I have one last word to leave you with.

The YNAB mixtape.

Honestly, the fact that this exists just makes my heart happy. I’m the idiot singing at the karaoke bar, sober, at 4 pm on a Tuesday. I’m a sucker for cover songs and love remixes (good or bad).

Luckily, the YNAB team has actually done a pretty incredible job.

If you just want to laugh, cry, smile, or hear the most absurd thing you’ve ever heard, be sure to check this out.

I’m talking Target shopping with Taylor Swift, Budgeting More with Justin Bieber, and YNAB-ING with Drake.

Even if you don’t ever use YNAB, these songs are worth a listen.

If You’re Still Not Sure

If after reading this insanely exhaustive review and listening to some T-Swift budgeting songs, you’re still not sure if YNAB will work for you, then leave a comment below.

I’ll do my best to answer any questions you may have, and if I can’t, I’m sure the YNAB support team would be happy to help.

Good luck, and no matter what you choose, remember that budgeting is an essential part of getting ahead financially. So just try and figure out a system that will work for you. If that system includes YNAB, great! If not, that’s OK too.

Best of luck!